Navigating the intricacies of GST returns is essential for businesses in India. One such critical return is the GSTR-1. In this article, we will discuss everything you need to know about GSTR-1 in detail to help you file GSTR-1 effectively.

What is GSTR-1?

GSTR-1, or Goods and Service Tax Return-1, represents the details of all outward supplies or sales made by a business in a given month/quarter. Every registered entity is required to file GSTR-1, even if their sales or outward supplies amount to zero.

Filing Period & Deadlines

- Period: Businesses with up to ₹5 crore annual turnover can opt for quarterly filing under the QRMP Scheme. While those with a turnover exceeding ₹5 crore must file the returns monthly.

- Deadline: Monthly GSTR-1 is due by the 11th of the following month, while quarterly filings are due by the 13th of the month after the quarter ends.

Eg. The GSTR-1 for the month of March should be filed by 11th April. Similarly, The GSTR-1 for the quarter of July – Sept should be filed by 13th October.

Exemptions from GSTR-1 Filing

Not all businesses need to file GSTR-1. Here’s who’s exempt:

1. Input Service Distributors (ISD):

These are taxpayers who:

- Get invoices for services used by multiple branches.

- Distribute the tax they’ve paid among those branches, ensuring each branch gets its fair share of the tax credit.

2. Composition Dealers:

A composition dealer is a registered taxpayer under GST who has opted for the composition scheme. Under this scheme, small businesses with a turnover of less than Rs. 1.5 crore can pay a fixed GST rate. This makes the GST process simpler for smaller businesses.

3. Suppliers of Online Information and Database Access or Retrieval Services (OIDAR):

Suppliers of OIDAR liable to pay tax themselves, as stipulated by Section 14 of the IGST Act, falling under this category are exempted.

4. Non-Resident Taxable Person:

This is for people or entities who sell goods or services in India occasionally & don’t have a regular place of business or residence in India.

5. Taxpayers Liable to Collect TCS (Tax Collected at Source)

6. Taxpayers Liable to Deduct TDS (Tax Deducted at Source)

Recommended Reads: 15 Best Invoicing Software In 2024

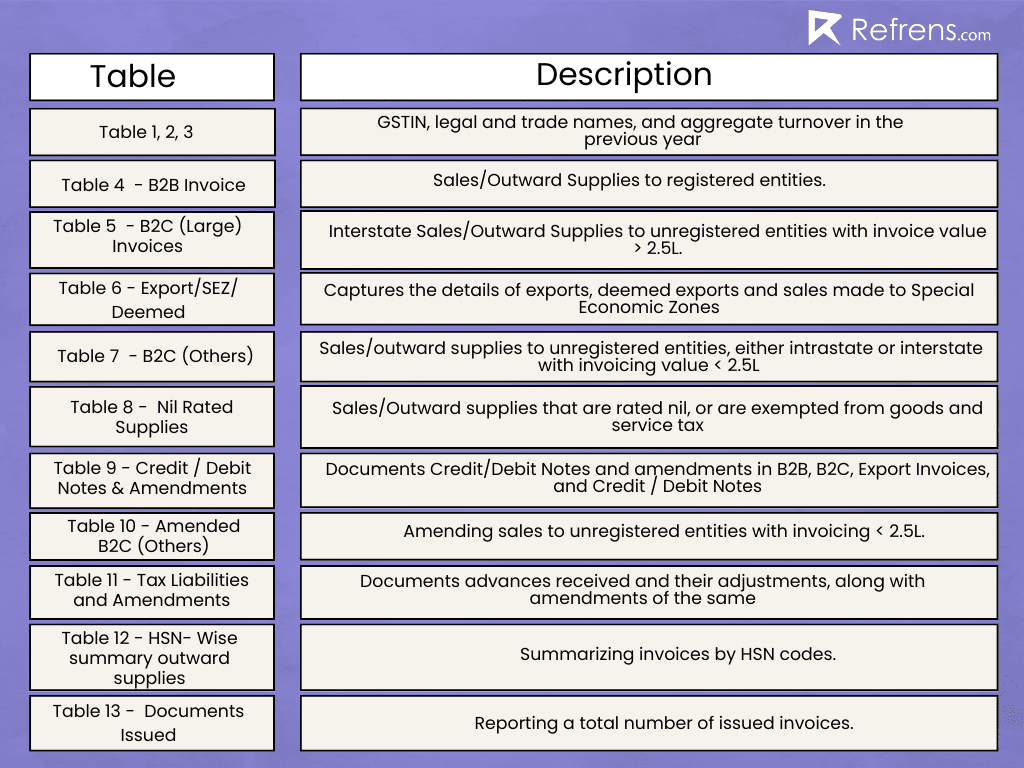

GSTR1 Sections

The entire GSTR-1 consists of 13 sections, divided into designated tables:

How to Amend GSTR-1?

Once a return is submitted under GSTR-1 it cannot be revised. However, if you discover an error in the return, you can correct it in the GSTR-1 of the subsequent period (either the next month or quarter).

How to File GSTR-1?

- Online: Through the GST portal.

- Offline: Using the offline utility tool

Tip: Platforms like Refrens can significantly simplify GSTR-1 preparation and filing. Their automated features ensure accurate, timely, and compliant submissions.

To file the returns offline, follow the given steps:

Step 1 – Click on Returns Offline Tool from the desktop, and the Returns Offline Home Page will appear.

Step 2 – Click on the NEW tab under ‘Upload new invoice/other data for return’

Step 3 – From the GST Statment/Returns drop-down list, select GSTR-1 and fill in your GSTIN, financial year, tax period, and aggregate turnover of the previous financial year and proceed.

The GST Offline tool zip file along with an Excel workbook will be downloaded which can be used to upload invoice data. The maximum number of invoice line items that can be uploaded is 19,000.

You are then presented with 4 options to upload the invoice data:

- Inputting the invoice information manually

- Uploading an entire Excel workbook comprising multiple sheets

- Copying and Pasting the content from the Excel Workbook

- Importing the CSV file

Create GSTR-1 in a few clicks, with Refrens!

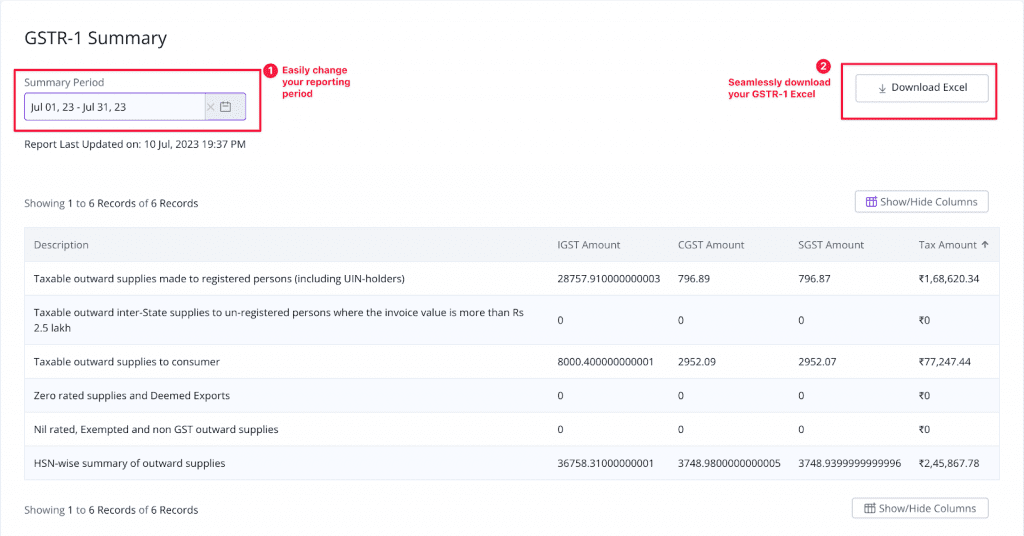

Top accounting software like Refrens can greatly help in simplifying your day-to-day accounting activities, including generating GSTR-1 reports.

Refrens automatically generates your GSTR-1 reports based on the invoices you create – so you don’t have to! If you are not using it already, you can just upload all your invoices in a few clicks & have your GSTR-1 ready to go.

Benefits of creating GSTR-1 using Refrens

- Simplified Tax Filing: You can prepare and manage your GSTR-1 reports in a much easier and more organized manner. It eliminates the need for manual intervention, making the process seamless and error-free.

- Time-Saving: By automating the process of generating GSTR-1 reports, you can save valuable time which can be invested in other aspects of your business.

- Compliance: Refrens’ GSTR-1 report feature will help you maintain compliance with the GST laws by ensuring you’re keeping up-to-date records of your outward supplies.

Read more: Top E-Invoicing Software in India: Detailed Analysis

Common Mistakes to Avoid When Filing GSTR-1

1. Incorrect Invoice Details: Precise entry of recipient invoice details in GSTR-1 is vital. Mistakes can deny input tax credits. Accurate invoice-level info matters.

2. Errors in Uploading Invoice Data in GSTR-1: GSTR-1 requires detailed data on outward supplies like invoice data, number, place of supply, tax rate, etc. Errors often arise due to the sheer volume of data, causing discrepancies between GSTR-1 and GSTR-3B. These mistakes impact reconciliation and can lead to penalties.

3. Ignoring Nil Return: It’s a common misconception that a NIL return doesn’t require filing if there are no transactions. But GST Law mandates the filing of a NIL return, even without sales or purchases. Skipping it can lead to penalties and even cancel GST registration.

4. Mixing Up Zero-Rated and Nil-Rated Supplies: Zero-rated and nil-rated supplies have different GST treatments. Nil-rated supplies have 0% GST, like exports or Special Economic Zone (SEZ) supplies but are not taxable, whereas Zero-Rated Supplies are taxable. Confusing them can complicate refunds. Precise reporting is crucial.

5. Forgetting Reverse-Charge Tax: Failure to fulfill reverse-charge tax obligations can result in interest payments and loss of input tax credits. It is crucial to pay reverse-charge tax via challan, as ITC cannot be utilized for this purpose.

6. Misplacing Export Sales: Export sales belong in the zero-rated supplies column, not regular sales. Misplacement can complicate GST refund claims.

7. Late or Missed Filing: Timely filing is key. Missing deadlines can cancel GST registration and result in fines.

8. Skipping Reconciliation: Forgetting to reconcile GSTR-1 (sales return) with GSTR-3B (summary return) can cause inconsistencies and inaccuracies.

Also read:

All Your Accounting FAQs Answered

E-invoicing In GST: A Complete Guide

Top 10 Inventory Invoice Software

Top 8 e-Way Bill Software

Top 10 Billing Software For Chartered Accountants

Top 7 Invoice Generator Software

Top Invoicing Software For Consultants

Billing Software For Export Business

Top Locksmith Invoice software

The Ultimate Guide to the Best Invoicing and Client Management Software

Top Accounting and Inventory Management Software for Businesses: A Comprehensive Guide

Related Posts:

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Everything To Know About GSTR 3

Everything To Know About GSTR 3

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 2A: How It Works and Why It Matters

GSTR 2A: How It Works and Why It Matters

GSTR 2: Everything You Need To Know

GSTR 2: Everything You Need To Know

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Everything to know about GSTR 9C: Eligibility, Filing Process, Amendments, and FAQS

Everything to know about GSTR 9C: Eligibility, Filing Process, Amendments, and FAQS

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

Complete Guide to GSTR 9A: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

GSTR 9B: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

GSTR 9B: Eligibility, Filing Process, Amendments, Mistakes to Avoid, and FAQS

A Comprehensive Guide to GST Compliance for E-Commerce Operators in India

A Comprehensive Guide to GST Compliance for E-Commerce Operators in India

GSTR 6A: Everything You Need to Know

GSTR 6A: Everything You Need to Know

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India