What Is Advance Tax?

Advance Tax is the income tax that individuals and businesses must pay in installments during the financial year, instead of paying it all at once at year-end.

It is often called the “pay-as-you-earn” tax system.

If the estimated tax liability for the financial year exceeds ₹10,000, you must pay advance tax in installments.

Who Has to Pay Advance Tax?

Advance tax applies to taxpayers with income from multiple sources. You must pay it if your tax liability is above ₹10,000 after deducting TDS.

✔ Salaried Individuals

Pay advance tax if you earn extra income like interest, rental income, or capital gains.

✔ Freelancers & Professionals

Designers, consultants, doctors, lawyers, and anyone receiving income without TDS must pay advance tax.

✔ Business Owners

Including proprietors, partnerships, LLPs, and companies.

✔ Presumptive Taxation Scheme (44AD/44ADA)

Taxpayers choosing presumptive income are not required to pay the quarterly advance tax. However, they must pay their entire advance tax by 15th March.

✔ Resident Senior Citizens (aged 60 or above)

Resident senior citizens are exempt from advance tax if they do not have any income from business or profession.

Why Is Advance Tax Important?

Paying advance tax helps:

- Avoid penalties under Section 234B & 234C

- Reduce financial burden at year-end

- Improve tax planning

- Improve compliance and cash-flow management

Advance Tax Due Dates

| Due Date | % of Tax Payable |

| 15 June | 15% |

| 15 September | 45% |

| 15 December | 75% |

| 15 March | 100% |

Note – For presumptive taxpayers (44AD/44ADA): Full amount is due by 15th March.

How to Calculate Advance Tax

The following steps would help to calculate the Advance Tax:

Step 1 – Estimate Annual Income:

Determine income from all sources, such as salary, business, freelancing, rent, and investments.

Step 2 – Deduct Allowable Deductions:

Subtract deductions under sections like 80C, 80D, and other applicable provisions.

Step 3 – Compute Taxable Income:

Subtract exemptions like HRA and deductions from the total income to arrive at taxable income.

Step 4 – Apply Tax Slabs:

Calculate tax liability based on the applicable income tax slab rates.

Step 5 – Account for TDS/TCS:

Deduct any tax already deducted at source (TDS) or collected at source (TCS) from your tax liability.

Step 6 – Determine Advance Tax Liability:

If the total tax liability exceeds Rs. 10,000 for the year, advance tax payments are required.

Step 7 – Divide Payments as per Schedule:

Split the calculated tax amount into instalments as per the prescribed due dates (June 15, September 15, December 15, and March 15).

Example of Advance Tax calculation

Let us consider an example to understand how advance tax is calculated:

Scenario:

Income Details:

Salary: Rs. 8,00,000

Freelancing Income: Rs. 5,00,000

Rental Income: Rs. 2,00,000

Deductions:

Section 80C (Investments): Rs. 1,50,000

Section 80D (Medical Insurance): Rs. 25,000

TDS Already Deducted: Rs. 50,000

Steps to calculate:

1. Calculate Total Income (in Rs.):

| Salary | 8,00,000 |

| Add: Freelancing | 5,00,000 |

| Add: Rental | 2,00,000 |

| Total | 15,00,000 |

2. Apply Deductions (in Rs.):

| Total Income | 15,00,000 |

| Less: Section 80C (Investments) | 1,50,000 |

| Less: Section 80D (Medical Insurance) | 25,000 |

| Taxable Income | 13,25,000 |

3. Calculate Tax Liability:

Using applicable slab rates:

| 0 to Rs. 2,50,000: 0% | 0 |

| Add: Rs. 2,50,001 to Rs. 5,00,000: 5% | 12,500 |

| Add: Rs. 5,00,001-Rs. 10,00,000: 20% | 1,00,000 |

| Add: Rs. 10,00,001-Rs. 13,25,000: 30% | 97,500 |

| Total Tax | 2,10,000 |

| Less: TDS | 50,000 |

| Advance Tax Liability | 1,60,000 |

4. Quarterly Instalment payments:

| 15th June | 15% of Rs. 1,60,000 | Rs. 24,000 |

| 15th September | 45% of Rs. 1,60,000 | Rs. 72,000 less Rs. 24,000 (already paid) = Rs. 48,000 |

| 15th December | 75% of Rs. 1,60,000 | Rs. 1,20,000 less Rs. 72,000 (already paid) = Rs. 48,000 |

| 15th March | 100% of Rs. 1,60,000 | Rs. 1,60,000 – Rs. 1,20,000 = Rs. 40,000 |

How to Pay Advance Tax Online

Advance tax can be paid easily through the Income Tax e-Filing portal:

1. Visit the e-Filing portal – https://www.incometax.gov.in/iec/foportal/

2. Click e-Pay Tax

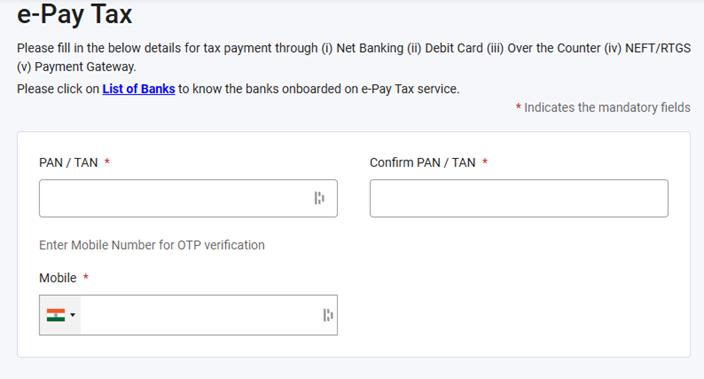

3. Enter the details below in the portal and confirm the OTP once you proceed.

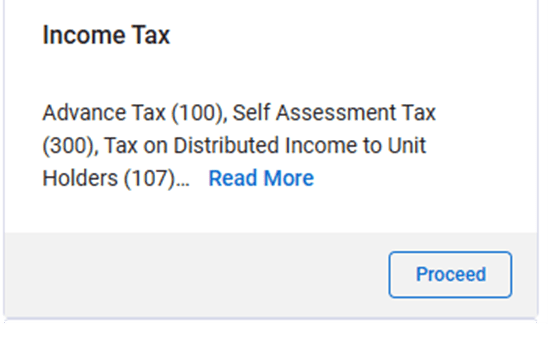

4. After your login, select Proceed at the Income Tax section.

5. Choose the Assessment year as 2026-27 and Type of Payment as Advance Tax(100)

6. Enter the tax amount in the below window

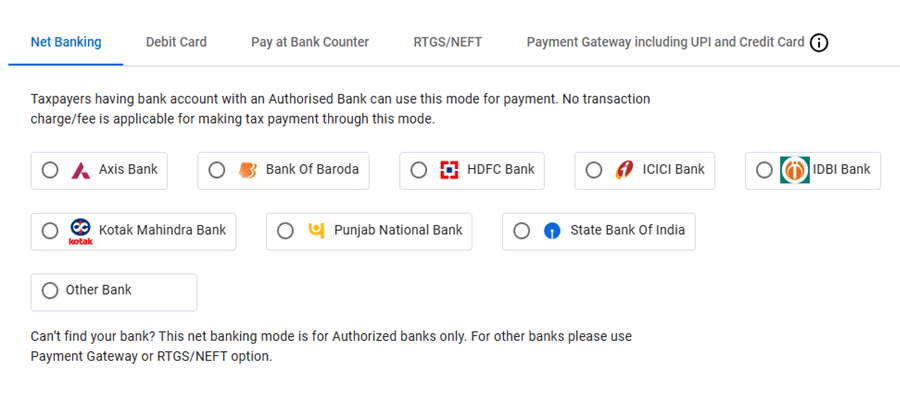

7. Make the payment using any of the below options

8. Once the payment is done, a challan will be generated, which can be downloaded and saved for the records.

What If You Don’t Pay Advance Tax?

You may face interest penalties:

1. Interest under Section 234B

By March 31, at least 90% of the total tax liability must be paid through advance tax or TDS/TCS. If this condition is not met, 1% interest per month will be charged on the unpaid amount until the payment is made.

2. Interest under Section 234C

If quarterly instalments of advance tax are not paid on time, interest is charged as follows:

| Scenario | Interest Rate | Duration | Basis for Calculation |

| Advance tax paid by June 15 is less than 15% | 1% per month | 3 months | Shortfall from 15% of total liability |

| Advance tax paid by September 15 is less than 45% | 1% per month | 3 months | Shortfall from 45% of total liability |

| Advance tax paid by December 15 is less than 75% | 1% per month | 3 months | Shortfall from 75% of total liability |

| Advance tax paid by March 15 is less than 100% | 1% per month | 1 month | Shortfall from 100% of total liability |

Penalties increase the overall tax burden; hence, timely payment of advance tax is essential.

FAQs

Q: Who must pay Advance Tax?

A: Anyone whose estimated tax liability for the year (after TDS) exceeds ₹10,000.

Q: What are the due dates?

A: You must pay by the 15th of June (15%), September (45%), December (75%), and March (100%).

Q: Are senior citizens exempt?

A: Yes, resident senior citizens (60+) are exempt unless they have income from a business or profession.

Q: What is the penalty for late payment?

A: You are charged 1% simple interest per month on the unpaid amount under Sections 234B and 234C.

Q: Do salaried employees need to pay it?

A: Yes, but only if they have significant non-salary income (like capital gains or rent) not covered by employer TDS.

Q: How do I make the payment online?

A: Use the Income Tax e-filing portal and select “Advance Tax (100)” as the payment type.

Q: What if I miss a deadline?

A: Pay the installment as soon as possible to minimize the 1% monthly interest accumulation.

Q: What is Section 234C specifically?

A: It is the interest penalty for failing to pay the required percentage (15%, 45%, 75%, 100%) by the quarterly deadlines.

Q: What is Section 234B specifically?

A: It is the interest penalty if you haven’t paid at least 90% of your total annual tax by March 31st.

About the Author

Kajal Agarwal is a qualified Chartered Accountant and Assistant Vice President – Finance at a U.S.-based multinational corporation, where she manages financial operations for clients generating over $100 million in revenue. A mentor to aspiring CAs and author of a widely acclaimed book on Company Law, she has also appeared live on DD News as a Budget 2025 expert, sharing insights on national fiscal policy. Outside her professional life, Kajal is deeply committed to holistic living as a long-time practitioner of Iyengar Yoga and a certified Pranic Healer, finding balance through yoga, meditation, and mindful leadership.

Related Posts:

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Everything To Know About GSTR 3

Everything To Know About GSTR 3

GSTR 7: Eligibility, Key Components, Penalties, and FAQs

GSTR 7: Eligibility, Key Components, Penalties, and FAQs

GSTR 7A: Eligibility, Downloading Process, Deadline, Mistakes to Avoid, and FAQS

GSTR 7A: Eligibility, Downloading Process, Deadline, Mistakes to Avoid, and FAQS

A Complete Guide to the Types of Invoices

A Complete Guide to the Types of Invoices

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

Your Complete Guide to GSTR 5: Filing Process, Due Dates, Penalties, Amendments, and FAQs

TDS & TCS Filing Deadlines FY 2025-26: A Complete Guide

TDS & TCS Filing Deadlines FY 2025-26: A Complete Guide

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Your Complete Guide to GSTR 4: Due Dates, Formats, Filing Process, Penalities, and FAQs.

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

Complete Guide to GSTR 8: Eligibility, Format, Procedure, Penalties, and FAQs

A Comprehensive Guide to GST Compliance for E-Commerce Operators in India

A Comprehensive Guide to GST Compliance for E-Commerce Operators in India

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

The Ultimate Guide to Inventory Management Metrics: Key Ratios, Costs, and Calculation Methods

The Ultimate Guide to Inventory Management Metrics: Key Ratios, Costs, and Calculation Methods

Everything to know about GSTR 9C: Eligibility, Filing Process, Amendments, and FAQS

Everything to know about GSTR 9C: Eligibility, Filing Process, Amendments, and FAQS

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

Complete Guide to GSTR 5A: Filing Process, Key Features, Penalties, and FAQs

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses