As the calendar turns to January 2026, the Indian taxation landscape is undergoing a tectonic shift. For nearly a decade, the Goods and Services Tax (GST) system relied heavily on “self-policing”, where businesses were expected to follow rules, and the government audited them years later.

That era has officially ended. Starting this month, the GST portal has transitioned into an automated enforcement engine. One of the most significant “ticking tax bombs” facing businesses today is the 180-day Input Tax Credit (ITC) reversal rule (Rule 37). For any invoices issued during the monsoon of 2025, the grace period is expiring. If your payments to suppliers aren’t settled, the system is ready to claw back your credits, with interest.

1. The Mechanics of the 180-Day Rule (Rule 37)

To navigate January 2026, we must revisit Section 16(2) of the CGST Act. While the law allows you to claim ITC immediately upon receiving an invoice and goods, that credit is technically “provisional.”

The Core Mandate

Under Rule 37, a recipient must pay the supplier the full value of the supply, including the GST, within 180 days from the date of the invoice. If you miss this window:

- Mandatory Reversal: You must add the claimed ITC back to your output tax liability in the GSTR-3B of the following month.

- Proportionate Reversal: If you made a partial payment, you only reverse the ITC corresponding to the unpaid portion.

2. Why January 2026 is the “Hard Enforcement” Era

In previous years, many businesses bypassed Rule 37 reversals, thinking they would settle it during an annual audit. However, two major portal updates in January 2026 make this impossible:

A. The Electronic Credit Re-claim and Reversal Statement

The GSTN has now fully operationalized the Reclaim Ledger. This statement tracks every rupee you reverse and every rupee you re-claim. Starting this month, the portal will issue automated alerts if your GSTR-3B claims do not match your ledger balance. If you try to re-claim credit that was never formally reversed, the system may block your GSTR-3B filing entirely.

B. Automated Late Fees and Interest

From January 1, 2026, the portal has moved toward auto-calculating interest under Section 50. If the system detects an unpaid invoice from 180 days ago that wasn’t reversed, it will calculate an 18% per annum interest liability automatically. This interest is a “dead cost” i.e. it cannot be claimed back even after you pay the supplier.

3. The “Utilization” Nuance

While the portal’s new automated systems are designed to flag every 180-day lapse, there is a critical legal nuance that could save your business thousands in interest: The Availment vs. Utilization Rule (Section 50(3)).

Following a retrospective amendment, the government clarified that interest is only triggered if you have both availed (claimed the credit in your return) and utilized (used that credit to pay your actual tax liability).

How to check if you owe interest:

Let’s assume you have claimed ₹1,00,000 ITC for an invoice in July’25 which wasn’t paid until Jan’26. Whether you need to pay interest or not can be checked as per below scenario –

- Scenario A (Safe): If you claimed the ITC but your Electronic Credit Ledger balance always remained higher than that amount, you haven’t “utilized” it.

In the above example – if the Electronic Credit Ledger balance for the entire duration of the aforesaid 180 days stayed above ₹1,00,000, you reverse the credit with zero interest.

- Scenario B (At Risk): If your ledger balance dipped below the credit amount because you used it to offset a monthly tax payment, you have “utilized” it. Interest at 18% will apply from the date of that utilization until the date of reversal.”

In the above example – if the Electronic Credit Ledger balance dropped to ₹80,000 in the month of Nov’25, the interest will be charged from Nov’25 till the ITC is reversed.

4. High-Risk Scenarios for 2026

Many businesses fall into the 180-day trap not because of a lack of funds, but due to commercial complexities. Watch out for these:

Retention Money in Infrastructure

In sectors like construction, it is common to hold 5–10% of the invoice value as “performance security.”

- The Trap: GST law does not recognize “retention” as an exception. If that 10% remains unpaid after 180 days, the corresponding 10% of your ITC must be reversed, even if the contract allows the delay

Disputed Invoices and Quality Issues

If you received sub-standard goods in August 2025 and withheld payment, you are still liable for reversal in January 2026.

- The Solution: You must ensure the supplier issues a Credit Note before the 180-day mark. A Credit Note reduces the “value of supply,” meaning no reversal is required for that amount.

Multi-Location Businesses (ISD)

As of April 2025, Input Service Distributor (ISD) registration became mandatory for businesses with multiple GSTINs under one PAN. If your Head Office received an invoice in July 2025 but didn’t pay the vendor, every branch that received a portion of that credit is now at risk of a system-driven reversal notice.

5. The “Double Whammy”: Blocked Filings and Suspensions

January 2026 brings even stricter “hygiene” checks on the portal. If your business is flagged for failing to reverse ITC under Rule 37, the consequences are cascading:

1. GSTR-3B Blocking: The system can prevent you from filing your current return until the “Negative Ledger Balance” is resolved.

2. E-Way Bill Disruption: If returns are blocked, you cannot generate E-Way bills, effectively halting your logistics and sales.

3. Automatic Suspension: The portal now monitors bank account updates. If your non-compliance is paired with outdated bank details, the system can automatically suspend your GST registration.

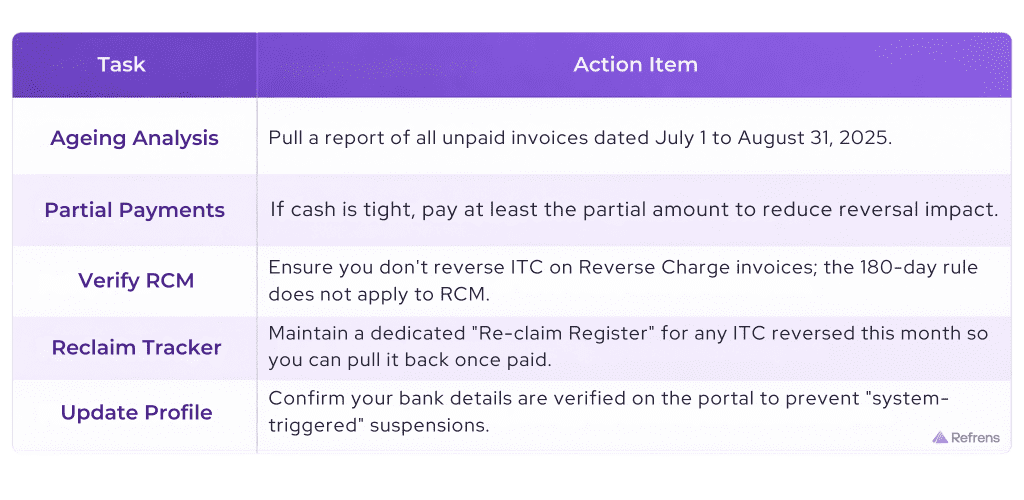

6. Practical Checklist: Protecting Your Business This Month

To avoid a tax shock, your accounts team should execute this January 2026 GST Audit:

7. The “Silver Lining”: The Re-claim Provision

While the 180-day rule is strict, the law offers a “re-entry” point. Unlike the strict deadlines under Section 16(4), which usually bar you from claiming old ITC after November of the next year; Rule 37 re-claims have no time limit.

If you reverse ₹1,00,000 of ITC in January 2026 because of a payment delay, and you finally pay that supplier in December 2027, you can re-claim that entire ₹1,00,000 in your December 2027 GSTR-3B. The only thing you lose forever is the 18% interest paid during the reversal period.

8. Frequently Asked Questions (FAQ)

Q1: Does the 180-day rule apply if the supplier hasn’t paid the tax to the government?

No, that is a different rule (Rule 37A). Rule 37 focuses solely on your payment to the supplier. If the supplier hasn’t paid the government, you may have to reverse ITC regardless of whether you paid the supplier or not.

Q2: Can I pay just the GST amount to avoid reversal?

No. The law requires payment of the “amount towards the value of supply along with tax.” You must pay the total invoice value.

Q3: Is interest applicable if I have enough balance in my Electronic Credit Ledger?

Yes. Following recent clarifications, if you “availed and utilized” the credit, interest is mandatory. If you merely “availed” it but never used it to pay taxes, you may be eligible for a waiver of interest upon reversal, but this requires careful documentation.

Q4: I claimed ITC on a July 2025 invoice but haven’t paid the supplier yet. If I reverse the credit in my January 2026 return, do I definitely have to pay 18% interest?

A: Not necessarily. It depends on your Electronic Credit Ledger balance between July 2025 and January 2026:

1. If your Ledger Balance stayed HIGH: If your total credit balance never dropped below the amount of that July invoice’s ITC, you have technically “availed” but not “utilized” the credit. In this case, you reverse the ITC in your January return with 0% interest.

2. If your Ledger Balance dropped LOW: If you used that credit to pay your monthly taxes and your ledger balance fell below the invoice’s ITC amount, you have “utilized” it. You must pay 18% per annum interest for the period starting from the date of utilization until the date of reversal.

About the Author: Kajal Agarwal is a qualified Chartered Accountant and Assistant Vice President – Finance at a U.S.-based multinational corporation, where she manages financial operations for clients generating over $100 million in revenue. A mentor to aspiring CAs and author of a widely acclaimed book on Company Law, she has also appeared live on DD News as a Budget 2025 expert, sharing insights on national fiscal policy. Outside her professional life, Kajal is deeply committed to holistic living as a long-time practitioner of Iyengar Yoga and a certified Pranic Healer, finding balance through yoga, meditation, and mindful leadership.

Related Posts:

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

Everything To Know About GSTR 3

Everything To Know About GSTR 3

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses

Understanding Reverse Charge Mechanism (RCM) Under GST: A Complete Guide for Businesses

GSTR 2A: How It Works and Why It Matters

GSTR 2A: How It Works and Why It Matters

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

GSTR 6: Filing Process, Eligibility, Recent Updates, and FAQs

Everything to know about GSTR 9C: Eligibility, Filing Process, Amendments, and FAQS

Everything to know about GSTR 9C: Eligibility, Filing Process, Amendments, and FAQS

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

A Quick Overview of GSTR-2B: Features, Benefits, and How to Use It

TDS & TCS Filing Deadlines FY 2025-26: A Complete Guide

TDS & TCS Filing Deadlines FY 2025-26: A Complete Guide

A Comprehensive Guide to GST Compliance for E-Commerce Operators in India

A Comprehensive Guide to GST Compliance for E-Commerce Operators in India

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Complete Guide to GSTR 9: Filing Process, Penalties, Tips, Mistakes to Avoid, and FAQs

Master GST Reconciliation: Process, Tools, and Best Practices

Master GST Reconciliation: Process, Tools, and Best Practices

GSTR 2: Everything You Need To Know

GSTR 2: Everything You Need To Know

A Complete Guide to the Types of Invoices

A Complete Guide to the Types of Invoices

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Everything To Know About GSTR-3A: Issuance, Actions to Take, and Consequences of Non-Compliance

Manufacturers’ Guide to Recovering 90% of IDS Refunds Quickly

Manufacturers’ Guide to Recovering 90% of IDS Refunds Quickly

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

GSTR: What is GST Return? Types, Rules, Procedures, and Penalties

Q4 Action Plan for Indian Business Leaders: 9 Proven Tactics to Finish FY26 on a High Note

Q4 Action Plan for Indian Business Leaders: 9 Proven Tactics to Finish FY26 on a High Note