Profit & Cash.

You may think these are synonymous with each other. That more cash means more profit, and vice versa.

But in reality, these are poles apart! A company with huge profits can be struggling with cash, whereas a company with huge losses might not.

If this makes you wonder why a profitable company might not have enough cash, then read further; this blog is the answer to that question!

In a successful business, the operations pay for themselves. For a business to run smoothly, its operations must sustain themselves, which can be impossible if its cash inflows and outflows don’t match in time.

In financial terms, it’s when your Debtors Receivable Days are higher than your Creditors Payable Days. This one imbalance drains liquidity from even the most profitable businesses.

The Lemonade Stand That Ran Out of Cash

Let’s understand this in simpler words. Say, Shreya, aged five, decides to run a lemonade stand as her summer project. She wants to learn business, make money, and buy herself a toy with her profits. So, she gets lemons, sugar, and cups from a vendor, and promises to pay for everything within two hours.

She sets up her cute stand on the street corner. Customers start coming in, love her lemonade, but most of them said, “I don’t have cash right now; I’ll pay you tomorrow when I come again.”

By evening, Shreya has sold 20 glasses of lemonade. Now the fruit vendor is asking for money. But her box is empty because all her customers promised to pay tomorrow.

Here, her receivables (money owed to her) are due tomorrow, but payables (money she owes to others) are due now.

So, she borrows some money from her elder brother, who lends it to her at a set interest rate.

If she doesn’t learn from her mistake, this vicious cycle will never end. Because the margin she earns on her lemonades will continue to be her brother’s interest income, and her dream of buying a toy for herself is gone.

The example sounds easy, but in real life, we have multiple vendors and multiple customers with different payment terms. So, how should we calculate the Debtor Receivable Days and Creditors Payable Days??

The calculation can be done using the formulas below –

| Debtors Receivable Ratio = Average Accounts Receivable / Credit Sales * 365 |

Where Average Accounts Receivable = (Opening Accounts Receivable + Closing Accounts Receivable)/2

And,

| Creditors Payable Ratio = Average Credit Payable/Credit Purchase*365 |

Where, Average Accounts Payable = (Opening Accounts Payable + Closing Accounts Payable)/2

And, Credit Purchases = Purchases of Stock-in-trade + Change in Inventories of Stock-in-trade

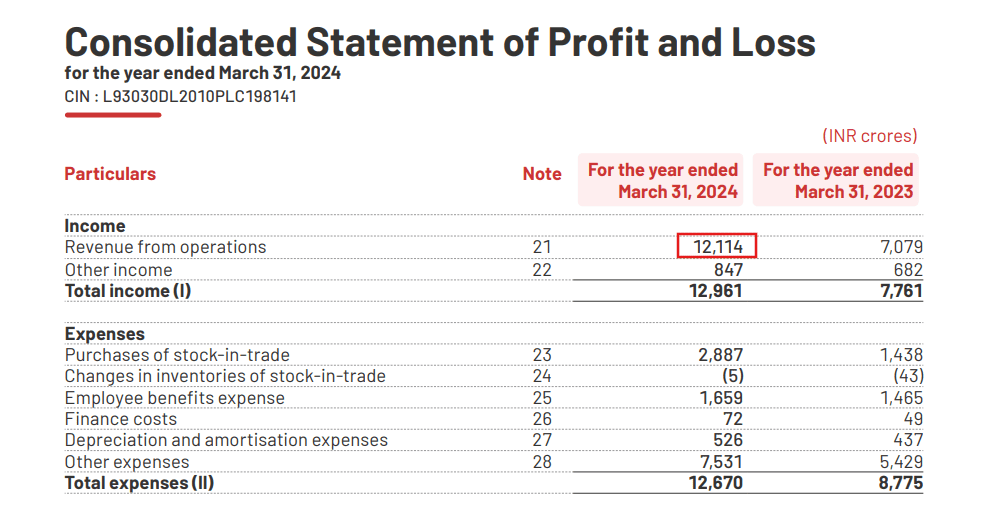

Let us understand with a real-life example, using the Financials of Zomato.

The Financials of Zomato can be downloaded from the link – https://b.zmtcdn.com/investor-relations/Zomato_Annual_Report_2023-24.pdf

Debtors Receivable Ratio

Debtors Receivable Ratio = Average Accounts Receivable / Credit Sales * 365

* For a company as big as Zomato, the entire sales is considered as Credit Sales

Here,

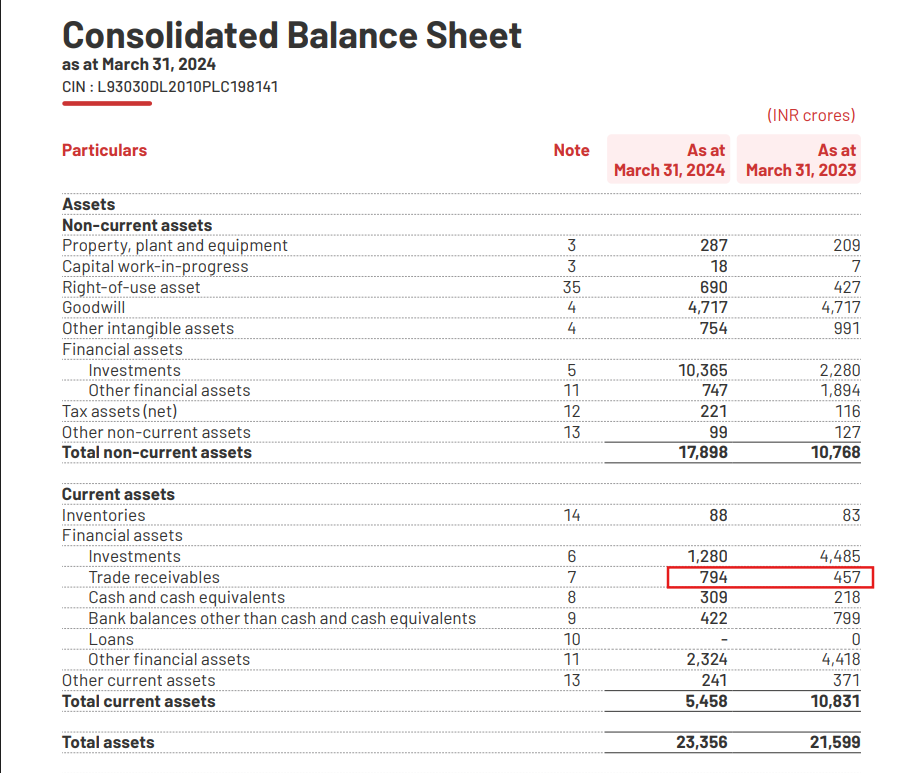

Opening Accounts Receivable (Trade Receivable) = 457

Closing Accounts Receivable (Trade Receivable) = 794

So, Average Accounts Receivable = 625.5 Cr.

So, to sum it all up –

| Zomato | Financial Data |

| Credit Sales* | INR 12,114 Crores |

| Average Accounts Receivable | INR 625.50 Crores |

| Debtors Receivable Ratio | 18.85 Days |

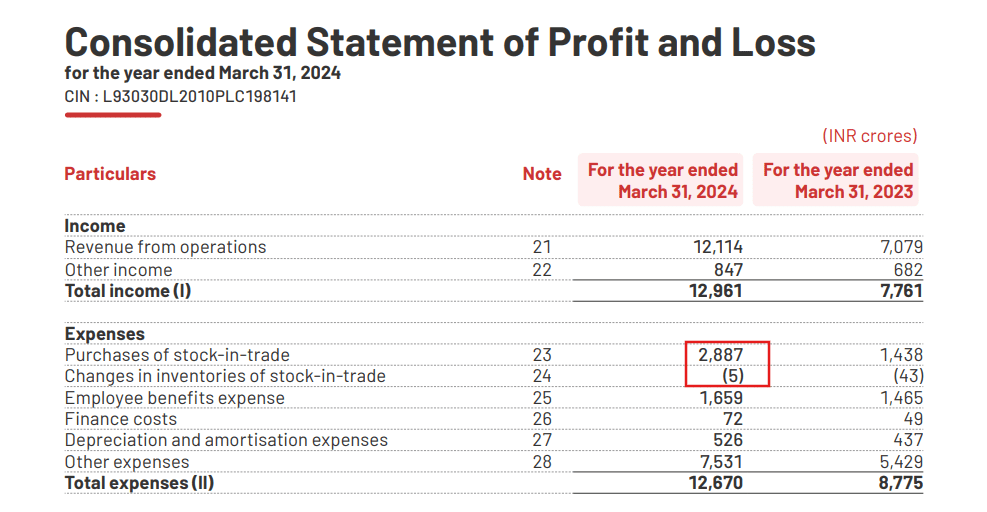

Creditors Payable Ratio

Creditors Payable Ratio = Average Credit Payable/Credit Purchase*365

Where, Average Accounts Payable = (Opening Accounts Payable + Closing Accounts Payable)/2

And, Credit Purchases = Purchases of Stock-in-trade + Change in Inventories of Stock-in-trade

Here,

Purchase of Stock in Trade = 2887

Changes in inventories of Stock in Trade = (5)

So, Credit Purchases = 2887 + (5) = INR 2882 Crores

Here,

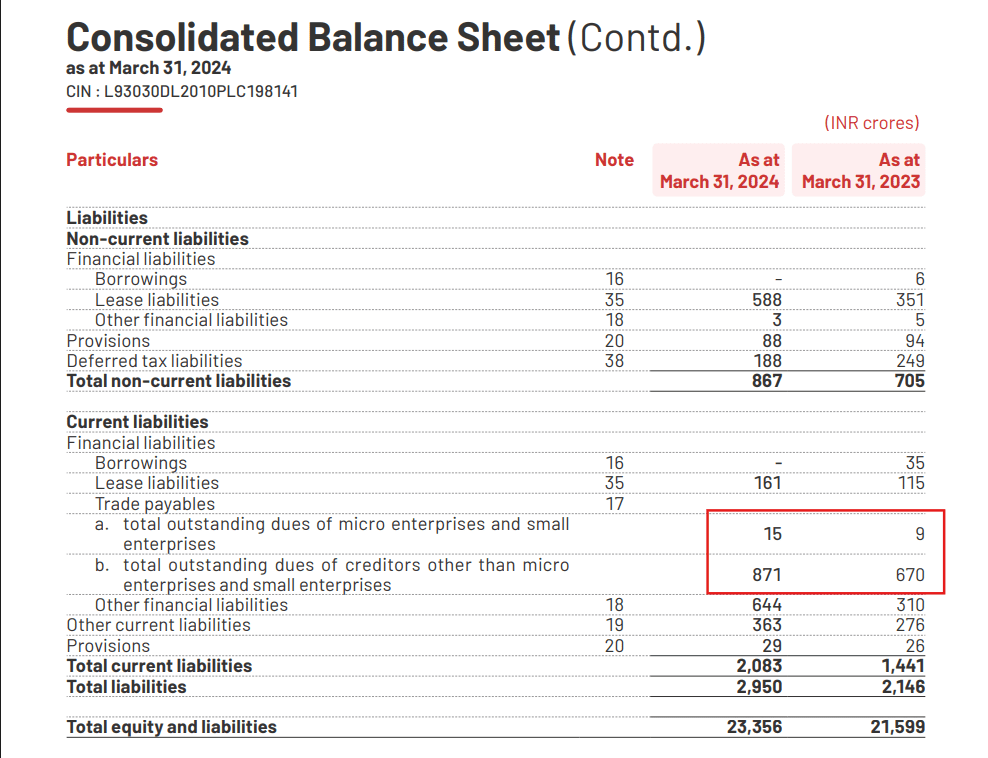

Opening Accounts Payable (670 + 9) = 679

Closing Accounts Payable (871 + 15) = 886

So, Average Accounts Receivable = 782.5 Cr.

So, to sum it all up –

| Zomato | Financial Data |

| Credit Purchases | INR 2,882 Crores |

| Average Accounts Payable | INR 782.50 Crores |

| Creditors Payable Ratio | 99.10 Days |

You can see that Zomato receives money from its Debtors in ~19 days; however, it pays its creditors in ~99 days, which helps in good rotation of the money from its Operating Business.

Zomato gets money from its customers almost 5 times before the payment is due to Creditors! Sounds like a dream for small and mid-size business owners!

The story is not only about Zomato! This trend will be visible in all the big companies, because they understand the fact that a Business can survive in the long run only if the Working capital churn is proper. The Creditors need to be paid from the money recovered from the Debtors and not through Loans.

The CFO Mindset: From Reactive to Predictive

We got to know the problem now! By having higher Receivable days, we are basically financing our own Customers.

But what about the solution? How can a small and mid-size company make sure that they don’t run into this trap?

Start small – Don’t aim at having leverage as Zomato does.

But instead, start with reducing the gap and ultimately making it zero. For instance, if your Receivable period is 45 days and Payable period is 30 days. We need to ensure that this gap is reduced. For ensuring that we can use the below methods –

1. Identify the customers to focus on through the analysis below –

1.1 Aging Analysis: Break down receivables by age brackets (0–30, 31–60, 61–90 days) to identify chronic delays. This will help in the identification of major customers where the focus needs to be.

1.2 Customer-Level Mapping: Identify the top 10 customers with the largest overdue amounts; often, 80% of your receivables come from 20% of clients.

✨For instance, Refrens‘ AI Assistant Freya will give you all these answers in seconds, without spending hours on Excel spreadsheets trying to analyze the data points.

A problem well-stated is half-solved. Once you know the focus area, the work becomes easier as we have a limited set of customers to focus upon!

2. The next step is to encourage customers to pay faster and nothing motivates quite like money.

Offer a 1–2% discount for early payments to make prompt settlement worth their while. Refrens has an inbuilt feature that lets you apply early pay discounts in literally just one click.

3. Once we have the current situation under control, next steps would be to place good Preventive measures in place in order to avoid running in the same situation again.

In order to do so, below measures can be adopted –

- Implement strict credit checks before onboarding customers and clearly state the credit limit available.

- Constant Follow-Ups using software like Refrens to ensure automatic follow-ups are done at regular intervals.

As we all know, a crying baby gets the milk! So, following-up is the key!

✨Refrens has a client and vendor onboarding approval system that helps you conduct KYC verification with real-time authenticity scoring. You can create multi-stage approval piplines tailored to your company guidelines.

✨Refrens also provides automated payment reminders so that you never miss a payment.

- Reward your sales team based on realized (collected) sales, not merely billed ones. This ensures they focus on bringing in quality customers who actually pay, strengthening both profitability and cash flow.

- Negotiate Longer Payable Terms – Suppliers, especially long-term partners, may agree to extended payment windows if you demonstrate reliability and volume potential.

Conclusion: Cash Flow Discipline Is the New Competitive Edge

In a high-interest-rate and credit-tightening environment, liquidity efficiency is the new profitability. Businesses that master their cash conversion cycle don’t just survive recessions; they expand when others contract.

If your receivable days exceed your payable days, you’re operating on borrowed oxygen – A sale isn’t a sale until the money is in the bank.

Fixing that imbalance is not just an accounting exercise; it’s a strategic imperative that determines whether your business thrives or merely survives.

About the Author

Kajal Agarwal is a qualified Chartered Accountant and Assistant Vice President – Finance at a U.S.-based multinational corporation, where she manages financial operations for clients generating over $100 million in revenue. A mentor to aspiring CAs and author of a widely acclaimed book on Company Law, she has also appeared live on DD News as a Budget 2025 expert, sharing insights on national fiscal policy. Outside her professional life, Kajal is deeply committed to holistic living as a long-time practitioner of Iyengar Yoga and a certified Pranic Healer, finding balance through yoga, meditation, and mindful leadership.

Related Posts:

The Ultimate Guide to Basics of Inventory Management

The Ultimate Guide to Basics of Inventory Management

The Ultimate Guide to Inventory Management Metrics: Key Ratios, Costs, and Calculation Methods

The Ultimate Guide to Inventory Management Metrics: Key Ratios, Costs, and Calculation Methods

Everything To Know About GSTR 3

Everything To Know About GSTR 3

Top Accounts Receivable Accounting Software (Updated 2025 List)

Top Accounts Receivable Accounting Software (Updated 2025 List)

Top 7 Inventory Management Software in Malaysia

Top 7 Inventory Management Software in Malaysia

Top 10 Inventory Management Software in Singapore

Top 10 Inventory Management Software in Singapore

Export Invoice: A Complete Guide for Seamless Trade

Export Invoice: A Complete Guide for Seamless Trade

Top 8 Inventory Management Software in India

Top 8 Inventory Management Software in India

A Complete Guide to the Types of Invoices

A Complete Guide to the Types of Invoices

Top 7 Inventory Management Software in UAE

Top 7 Inventory Management Software in UAE

Top 10 Inventory Management Software in the UK

Top 10 Inventory Management Software in the UK

GSTR 2A: How It Works and Why It Matters

GSTR 2A: How It Works and Why It Matters

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Your Complete Guide to GSTR 3B: Filing Process, Due Dates, Penalties, and FAQs

Top 10 Inventory Management System in the USA

Top 10 Inventory Management System in the USA

Top 6 Inventory Management Software in Indonesia

Top 6 Inventory Management Software in Indonesia

Top 7 Inventory Management Software in Australia

Top 7 Inventory Management Software in Australia

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

Mastering Input Tax Credit (ITC) Under GST: A Comprehensive Guide for Businesses in India

Comprehensive Guide to Sales Orders

Comprehensive Guide to Sales Orders